Tharp's Thoughts Weekly Newsletter (View On-Line)

-

Article SQN® Optimization by Means of Step-Forward Testing, Part 2, by Douglas Rechia

-

-

Trading Tip Don’t Throw the Baby Out with the Bath Water, Part 2,

by D.R. Barton, Jr.

Peak Performance Workshops May 2012

Learn to trade with less stress and more profitably through proper preparation and psychological conditioning. If you lack a solid trading plan and get stressed out when you trade, you’ll naturally tend to cut your profits short and hold on to losers. Both of these workshops help traders address this “normal” bias to lose in the markets in complementary ways.

SQN® Optimization by Means of Step-Forward Testing SQN® Optimization by Means of Step-Forward Testing

Part 2: The Results

by Douglas Rechia, M.Sc

In last week’s newsletter (click here), I explained the SFT process and the setup for my experimental test of a simple trend-following trading system for stocks in the Ibovespa index. I said I was going to optimize on two parameters—number of days to identify a trend in an individual stock, and the ATR multiplier used for the stop. My optimization metric was the SQN® score for the system results. The following are the results from that process (Editor's Note: In Part 1 of this article, the following statement should have been added to Trend-I rule number 2: “Calculate entry price and initial stop loss. Enter only if entry price is higher than initial stop loss.” Click here to see the amended rule).

SFT Results Analysis

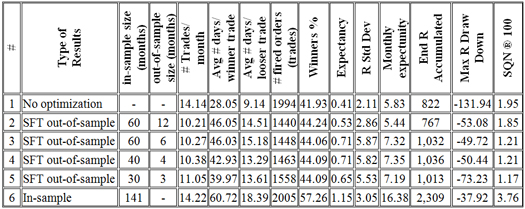

The accumulated out-of-sample data results for each Ibovespa stock were saved, and the overall results from January, 2000 to October 18th, 2011 are presented in Table 1.

Table 1: The Impact of Optimization on Trend-I

View Larger Image

Test 1 used no optimization, fixing the parameters c and d at 25 and 3, respectively. Tests 2 through 5 varied the size, in months, of in-sample and out-of-sample data (see third and fourth columns) with optimized parameters. Test 6 was the backtest result using the optimal parameters selected by massive testing in the same period. Test 6 had no practical value because it's just the optimal result from past data. However, it serves as a benchmark reference for the others because it shows the maximum potential gain from the rules adopted by the system. Note how impressive the in-sample numbers are: 14 trades per month, 57% of the trades are winners, expectancy is 1.15R, SQN® 100 is 3.76 and max R drawdown is only about -38R. In an ideal world, the trader would have a “magic trick” that gives a clue beforehand about the optimal parameters that provide results close to the in-sample test 6.

Normally, the in-sample tests perform much better than out-of-sample tests; otherwise, the trader is probably optimizing the wrong parameters or there is some flaw in the optimization process. If a system optimization has been well designed, the parameter values selected by in-sample tests in distinct data intervals will vary to some extent. If, however, unoptimized and optimized performance results are very similar, the system may not be worthy of optimization work.

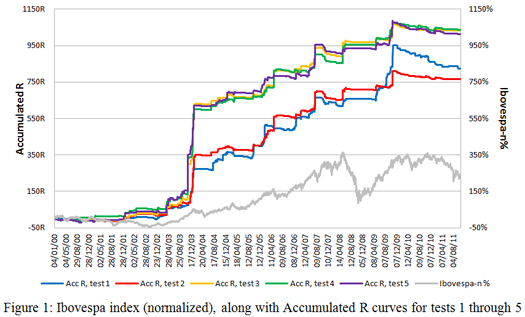

Now, let’s revisit the “real” world and focus on out-of-sample validations 2 through 5. Surprisingly, the SQN® scores for all of the out-of-sample validations are lower than the non-optimized test 1 SQN® score. Other measures of system performance, however, including max R drawdown, expectancy, winning trade % and total accumulated were noticably better. Figure 1 depicts the evolution of the accumulated R curve for each test through time. The right-hand scale shows the normalized Ibovespa rate of change.

View Larger Image

Clearly, we see a high correlation in tests 3, 4 and 5 with very similar accumulated R curves for these three. On the other hand, by doing just one optimization a year, as it was done in test 2, the performance degrades too much. It seems that one optimization every 4 months, like test 4, is fine.

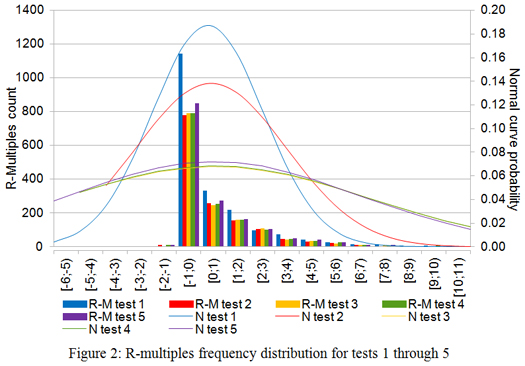

Figure 2 represents another way to analyze the same data by looking at the frequency distribution of the trades in tests 1 through 5. The mean and standard deviation for each test were plotted using an assumed normal distribution. The cumulative amount per R-multiple trade result is plotted against the primary axis (left), and the distribution curves are against the secondary axis (right).

I had expected the SFT optimization process to yield higher SQN® scores, but instead, the SQN® scores were lower than the non-optimized test 1. Why? Figure 2 provided me with insight as to why. The SQN® is based on a statistical test for normality. The optimized parameters did provide higher expectancy results and lower drawdowns, but they accomplished this through less “normal” results—and therefore generated lower SQN scores.

For example, test 1’s distribution (the blue bars) appears to be closer to a normal curve than test 4’s (the green bars). Test 1’s standard deviation is lower than test 4’s (see Table 2), so test 1 has a higher SQN®. Test 4’s higher standard deviation is due to some very high positive R-multiple trades that caused a higher variance in the distribution (according to Van Tharp in The Definitive Guide to Position Sizing ™, this is a well-known attribute of the SQN® score).

Using the results of the SFT optimization process, I applied a position sizing strategy to the test parameters and ran an equity simulation. When I did that, however, I saw no correlation in the equity curves for tests 1 through 5. Tests 3, 4 and 5 still provided the top 3 highest-ending equity amounts, but the individual signals from each of those tests produced very different equity curves.

How SFT Helped Me Understand Trend-I

In a nutshell, SFT helped provide some important knowledge about Trend-I performance.

- More than a 60% reduction in drawdown size—the max R drawdown was reduced from the unoptimized -130R (test 1) to about -50R (test 4).

- Trend-I caught the principal bull markets, including the one in 2009; Trend-I was out of the market during the 2008 financial crisis.

- Trend-I started holding positions close to the beginning of the bull markets and getting out a little after the main tops.

- The sideways market in 2010 caused lots of whipsaws in the accumulated R curves.

- The sharp upward direction of the accumulated R curves (see Figure 1) from tests with out-of-sample data shows that, in general, Trend-I did not overfit past data, but used in-sample quotes to select the system parameters that were useful to improve the overall system performance.

Unoptimized, Trend-I provided consistent, ordinary trend-following-type returns over time. The SFT process clearly helped improve system performance through parameter optimization.

Even though SFT yielded lower SQN® scores, I am satisfied with the results of the optimization process. I see that the lower SQN scores resulted from the higher standard deviation as a result of a few large R multiple trades, but the optimizations did not seem to increase the size of the losing trades by much at all. I will have to decide how those lower SQN scores affect my position sizing strategy as I move forward.

I believe the Monte Carlo analysis confirmed my hypothesis that the optimized systems are more likely to help me achieve my objectives than the non-optimized system. I plan to confirm this hypothesis in the next few months with position sizing simulations and trading a demo account.

Acknowledgments: I am grateful to the authors of the many books on trading that I have read. Although I’ve never met them, I acknowledge the contribution of Van Tharp and Perry Kaufman to this work. I also want to thank Tharp’s staff for their help with editing this article. Thank you for your valuable support!

About the Author: Douglas N. Rechia is an experienced computer programmer, software architect and designer. He lives in Florianópolis, a small island city in the South of Brazil. About two years ago, he decided to apply his computing skills to the markets. He welcomes comments from readers as he has not yet put his experimental systems into production. You can reach him at rechia (at) gmail.com.

Disclaimer

Trading Education

Workshops

We have two new workshops added to our line-up!

- Forex Trading. This is the three-day version. Last year, our one-day version sold out, and we had to create a waiting list.

- We've added a new Tharp Think event. This is a one-day sampling of Van Tharp's workshops, and it's only $299.

The rest of the line-up consists of our time-tested favorites. Click on the title of the workshop below to find out more.

May

17-19 |

$2,295

$2,995

|

Peak Performance 101

Van Tharp's Signature Workshop |

Cary, NC |

May

21-24 |

$3,295

$3,995

|

Peak Performance 202

with Dr. Libby Adams |

Cary, NC |

| June 2 |

$299 |

Tharp Think

Your chance to get a taste of a Van Tharp workshop for only $299 |

Cary, NC |

June

14-16 |

$3,295

$3,995

|

Forex Trading

New! Three-Day Workshop |

Cary, NC |

June

18-20 |

$2,295

$2,995

|

How to Develop A Winning Trading System That Fits You

with Van and RJ Hixson |

Cary, NC |

August

24-30 |

$5,090

(combo)

|

Peak 101 and Peak 203 (AKA, The Happiness Workshop) |

Cary, NC |

| Sept 21-28 |

Varies |

Mechanical Systems for Day and Swing, and Discretionary Live Trading |

Cary, NC |

To see our full workshop schedule, including dates, prices and location, click here.

Now posted, dates for Aug-Oct!

Trading Tip

ETPs—Don’t Throw the Baby Out with the Bath Water ETPs—Don’t Throw the Baby Out with the Bath Water

Part 2

by D.R. Barton, Jr.

Over the past couple of weeks, we’ve been discussing the pluses and minuses of Exchange Traded Products (ETPs) in the form of Exchange Traded Funds (ETFs) and Exchange Traded Notes (ETNs).

To recap, we’ve reviewed some of the quirks about ETPs that must be understood if we want to avoid getting caught in rare traps, like paying a large premium for ETNs that have suspended new share creation. Aside from their minor weaknesses, ETPs are incredibly useful as trading instruments in all time frames. Last week, we saw that institutions, individual traders and investors agree: ETPs dominate any list of highest-volume stocks.

Since so many people are using these instruments to trade and invest, I thought it would be useful to talk about choosing among similar ETPs. For example, if your research led you to the conclusion that the energy sector should move higher, what ETP should you buy? Or if you thought residential home builders were ripe for another move up, what ETP should you use to express that idea?

Choosing ETPs: Make Sure You Know What You’re Buying

As we’ve said before, ETPs are just basically baskets of stuff—mostly stocks or futures contracts. To really understand what you’re getting when you buy an ETP, you have to look beyond the name and dig into what they own. Let’s dig into the issue of choosing an ETP that can grow if the residential real estate market rebounds.

Let’s say we want a real estate ETP—specifically, one that tracks home builders. There are plenty to choose from and a number of free websites to help you find them. I happen to use one called etfdb.com that provides the kind of useful information we’re seeking for this exercise. It provides all the ETPs related to real estate, or home building, or a specific geographic region, etc.

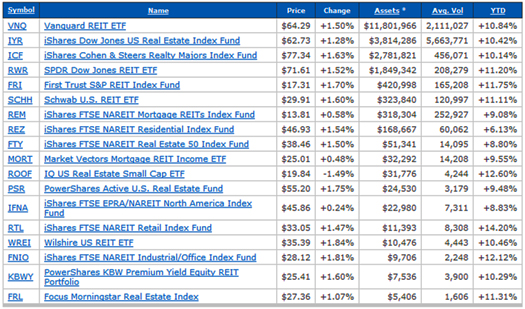

If you look at the real estate ETPs on the etfdb.com site, you’ll see the following list:

View Larger Table

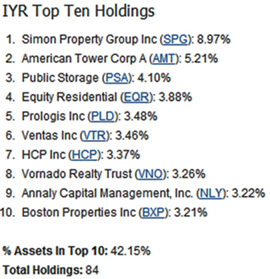

If we were looking for exposure to residential real estate, we’d probably suspect that the ETPs with REIT (Real Estate Investment Trust) in the title are not what we want. But what about IYR—the most heavily traded ETP in the list? Its full name is “iShares Dow Jones US Real Estate Index Fund.” To see if this is the ETP we want, we need to find out what stocks are in its basket by clicking on the name. Here’s what etfdb.com lists as the top 10 holdings for IYR:

Without much digging, we’ve discovered that this particular ETP is slanted more toward commercial real estate and commercial management. Not what we’re looking for.

If we look further down the ETP list, we find the symbol REZ, or “iShares FTSE NAREIT Residential Index Fund.” Maybe that’s the one we’re looking for. Before we look at its top holdings, though, let’s take a peek at the description for this fund: “Description: The index measures the performance of the residential real estate, healthcare, and self storage sectors of the U.S. equity market.” We don’t want health care and self storage. Have we hit a dead end?

Let’s try something different. Perhaps we can find what we’re looking for in another category listed on etfdb.com—building and construction.

View Larger Table

Finally! It looks like we’ve hit pay dirt. Before jumping in with both feet, though, we need to look at the holdings for these ETFs. The second two look too broad (and they’re very thinly traded), but the first two look promising, especially XHB, or “SPDR S&P Homebuilders ETF.” However, when we look at the top holdings, we find this:

Wow—the only true home builder among this ETF’s top ten holdings is Lennar! The others are building materials companies like USG (wall board), Masco (plumbing and cabinets), Owens-Corning (insulation) and retail stores like Bed Bath & Beyond and Williams-Sonoma that cater to home owners!

We still have one last chance. ITB—the US Home Construction Index—has a pretty broad title, so it could be anything. Looking at the top holdings, we see:

Finally! Home builders galore! If we want exposure to residential builders—especially home builders—then the ITB is our ticket. Six of its top seven holdings are home builders. The ETPs in both the real estate and building and construction sectors, well, not so much…

Next week, we’ll dig into some of the vagaries of investing in the energy market through ETPs.

As always, I’d love to hear your comments and feedback. Send them to drbarton “at” vantharp.com.

Great Trading, D. R.

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured guest on both Report on Business TV, and WTOP News Radio in Washington, D.C., and has been a guest on Bloomberg Radio. His articles have appeared on SmartMoney.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Disclaimer

Peak Performance Home Study Program for Traders and Investors

YOU are the most important factor in your trading success!

You create the results you want. Going through this home study course, you’ll gain a perspective on the "how" and "why" of your past trading results and learn techniques to increase profits and reduce stress.

Your success as a trader depends upon the amount of work you put into applying the principles of the course to your investing and trading. Get started now and take charge of your trading success!

Learn More

Buy Now

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Click here to take our quick, 6-question survey.

Also send comments or ask Van a question by using the form below.

Click Here for Feedback Form »

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, click here

To stop your subscription, click on the "unsubscribe" link at the bottom left-hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute

Back to Top |

|

April 25, 2012 - Issue 574

A Must Read for All Traders

Super Trader

How are we doing?

Give us your feedback!

Click here to take our quick survey.

From our reader survey...

"I think the newsletter is extremely generous and it is a resource I utilize constantly. I have saved every single one since I first subscribed."

Trouble viewing this issue?

View On-line. »

Tharp Concepts Explained...

-

Trading Psychology

-

System Development

-

Risk and R-Multiples

-

Position Sizing

-

Expectancy

-

Business Planning

Learn the concepts...

Read what Van says about the mission of his training institute.

The Position Sizing Game Version 4.0

Picking the right stocks has nothing to do with trading success and neither do amazing trading systems with high percentage wins. The Position Sizing Game teaches you the key elements of trading success. Learn more.

To Download for Free or Upgrade Click Here

Download the 1st three levels of Version 4.0 for free.

Register now. »

Trouble viewing this issue?

View On-line. »

A Thousand Names for Joy: A Commentary

You can read Super Trader Curtis Wee's full review here.

Dr. Tharp is on Facebook

Follow Van through

Twitter »

Van Tharp Trading Education Products are the best training you can get.

Check out our home study materials, e-learning courses, and best-selling books.

Click here for products and pricing

What kind of Trader Are You? Click below to take the test.

Tharp Trader Test

Back to Top

Introduction to Position Sizing™ Strategies

E-Learning Course

Only $149

Learn More

Buy Now

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute |