Tharp's Thoughts Weekly Newsletter (View On-Line)

-

Article How Big Could My System's Max R Multiple Drawdown Be? by R.J. Hixson

-

-

Trading Tip An Update on the August Market Doldrums by D.R. Barton, Jr..

-

Only Two Weeks Away,

Oneness Awakening Weekend - August 10-11

Spend two full days with Van and learn how you can become more aware, positive, calm, centered, and successful. This will likely be a special event as Van is just returning from a powerful Oneness Summit in India and will be brimming with new ideas! Van considers this such a powerful process for transformation he even allows it as an entry point to be considered for Super Trader Program.

Only $195. To learn more or register, click here.

How Big Could My System’s Max R Multiple Drawdown Be? How Big Could My System’s Max R Multiple Drawdown Be?

by R.J. Hixson

View On-line

We are in the process of finishing off the second edition of Van’s "Definitive Guide to Position Sizing Strategies." The vast majority of readers of the first edition said they were generally very satisfied with the book as it was. There was still room for improvement, of course, so that’s why Van updated material for the second edition.

We have a bit of research that did not make it into the second edition. It’s only in its initial stages and depending on priorities, it may remain as a side research project for some time more. Even still, you may find either the process or the tentative results interesting.

What's My System's Max R Multiple Drawdown?

From time to time, clients email or call in with this question, however, a conversation earlier this year sticks out in my mind. I was speaking with a former floor trader in Chicago who was working on this question for his own trading and really wanted to figure it out. In the conversation, he asked something like, “How many people do you know that have been struck by lightning and lived?” Personally, I didn’t know anyone, but he did. Actually, he knew someone that had been struck by lightning twice—and lived. He believed knowing his max possible drawdown was critical to his trading given his life experiences.

Even if you don’t know anybody that has been struck by lightning, knowing with some confidence your trading system’s max R multiple drawdown would be useful. In the past, the best way to figure that out was by using a trading system simulator. One of the objectives for The Definitive Guide book, however, is to help people come up with effective position sizing strategies without needing to use a simulator. So how might we help traders figure out what their max drawdown might be?

The Process

Could there be a way to estimate the max drawdown for a trading system with only some basic information which most traders would already have or could easily calculate? That would require a set of beliefs that some relationship exists between trading system R multiple distributions and the max drawdown size. Is that so or could that be so?

To get an idea of what the maximum drawdown would be for a trading system, we generated 33 different trading system R multiple distributions. For the sample of 33 systems, we systematically varied the R multiple distribution’s characteristics including:

- winning percentage of trades (range of 10% to 90%)

- average win size and maximum win size (.23R to 95R)

- average loss size and maximum loss size (-1R to -2.5R).

We simulated the distributions for 1,000 trade runs 10,000 times which generated the following statistics:

- expectancy (which ranged from +.10 to +8.51)

- R multiple standard deviation (.37 to 28.68)

- mean losing streak length, median losing streak length (1.7 to 27.1 trades)

- maximum losing streak length (5 to 99 trades)

- SQN score, SQN 100 score (1.0 to 6.0)

- maximum R multiple drawdown at 95% confidence level (-4.2R to -46R)

- maximum R multiple drawdown (-10R to -99R)

Afterwards, we looked at the correlations among all of the variables above. We ran a multiple regression analysis on about a dozen combinations of different variables with very low or no correlations in order to test which ones would be most helpful in calculating the max R multiple drawdown figure. One set of four variables came out with an R square value of .98, or in other words, we could have high statistical confidence that that particular combination of variables and weightings “worked” pretty well. The best combination of variables for estimating the maximum drawdown included these four:

- Expectancy

- R multiple standard deviation

- Winning percentage

- Average loss

The Max Drawdown Equation

Here’s the equation:

R multiple drawdown @ 95% confidence level =

(26.6 x the average R multiple loss (a negative number)) + (13.7 x expectancy) + (21.6 x winning percentage) - (5.0 x R multiple standard deviation) + 4.1

Example —

System A

Average R multiple loss = -1.0R

Expectancy = .42

Winning percentage = 50%

R multiple standard deviation = 1.47

Here’s some additional data about this system -

Maximum loss size = -1.5R

SQN100 score = 2.9

Average losing streak (simulated) = 6 trades

Max losing streak (simulated) = 19 trades

So, using this system’s information to fill in the numbers yields:

(26.6 x -1) + (13.7 x .42) + (21.6 x .5) – (5 x 1.47) + 4.1 = -13.3

The equation estimates a -13.3R maximum drawdown at the 95% confidence level. This compares to the “actual” result from the 10,000 simulations of -12.6R at the 95% confidence level. For this system, the equation's max DD estimate is 105.6% of the simulated result — within 6% of the “actual” simulated results.

Interestingly, the maximum drawdown from all of the simulations was usually somewhere around twice the amount of the max drawdown at the 95% confidence level.

Caveat Mercator! (Loosely Translated: Let the Trader Beware!)

Before we get to how you might use the equation, let’s review a list of important limitations to consider before applying it.

- The sample of simulations is just barely big enough to be statistically significant.

- The sample of simulations may have been less than systematically varied.

- Two different trading system simulators did not agree on the size of the max drawdowns — we favored the simulator with more “consistent” results based in part on the advice of a consulting PhD in statistics.

- There were no real world trading system results used for the simulations or regression analysis.

- Possibly unknown biases or errors in the logic, coding, data, and analysis affected the results — as they do with any research like this.

- The equation seemed to generate significantly different maximum drawdown figures than the simulated maximum drawdown figures for systems with higher SQN scores (5 and above).

- None of the systems tested had R multiple losses greater than -2.5R. Many of the systems had a max trade loss size of -1R.

- The equation seemed to work decently for systems that had a distribution with a “somewhat normal appearance” (i.e. the distribution histogram had a hump somewhere in the middle of the results even if it was skewed to one side). The equation seemed to estimate the max DD poorly for systems with distribution histograms that appeared nearly flat or “V” shaped.

- The equation estimate for drawdowns ranged from between 80% and 118% of the drawdowns that the simulations generated. 90% of the equation estimates were within 14% of the simulated drawdown results and 40% of them were within 5%. We were able to partially explain (theorize really) the equation’s outlier results or poor estimates, but could not theorize why some of the other, less dramatic variations occurred.

Given all of these limitations, you might be wary of using the equation. Your wariness is quite justified at this point. There’s no voodoo here, but clearly, better understanding the system performance interrelationships so you can better estimate a max DD figure will require some more work on our part. For lack of anything short of running a full trading simulation, however, the equation could give you at least some idea of what a max drawdown might be.

How To Use This Information

If you have a trading system that has performance parameters within the ranges that were tested above, you might use the equation to provide some guidance for estimating a maximum R multiple drawdown. (Avoid believing, however, that this equation “determines” your maximum R multiple drawdown.) You could then use the max R multiple DD estimate and your risk amount ($) to help ensure your position sizing strategy keeps you from hitting your maximum equity drawdown — assuming you have that objective defined (which you should).

If you have a trading system with parameters beyond those listed above that were simulated, it would be best to avoid using this equation at all.

If you have any feedback on this process or the results, feel free to email it to us at [email protected]. We will make an announcement in this newsletter in the coming months when the second edition of the Definitive Guide to Position Sizing Strategies is hot off the press!

Thank you for your thought and attention.

About the Author: R.J. Hixson is a devoted husband and active father. At the Van Tharp Institute, he researches and develops new products and services that help traders trade better. He took a bit of Latin in high school but remembers better his spoken French lessons. He can be contacted at “rj” at “vantharp.com”.

Trading Education

Three Weeks Away From The Day Trading Workshop

Ken Long teaches the FROG trading system and the RLCO (regression line crossover) system. You'll trade the FROG via a trading simulator, offering you the equivalent of many hours of trading experience. Ken will exhibit numerous case studies of RLCO trades in simulated real-time using recorded ticks. Then to further expand your experience trading these systems, stay on for the three days of optional live trading.

At current registration rates, we expect to sell out. In addition, the $700 early enrollment discount is ending soon. Register now.

| August 10-11 |

Oneness Awakening Weekend

with Van Tharp |

August 16-18 |

Day Trading Systems

with Ken Long

|

August 19-21 |

Live Day Trading

with Ken Long

Day Trading Systems is a prerequisite to this course. You'll trade alongside Ken for 2-3 days.

|

October 3-5 |

Peak Performance 101

with Van Tharp |

Special Location: Berlin, Germany

Van does not go to Europe every year, so be sure to catch him in a few months in Europe! |

September 6-8 |

How to Develop a Winning Trading System

with Van Tharp and RJ Hixson

|

September 10-12 |

Blueprint for Trading Success

A step-by-step process (blueprint) for pulling all of the important elements of successful trading together into one cohesive plan. |

September 14-16 |

Forex Trading

with Gabriel Grammatidis

|

Register for all 3 and save $800!

|

To see the full schedule, including dates, prices, combo discounts and location, click here.

Trading Tip

An Update on the August Market Doldrums An Update on the August Market Doldrums

by D. R. Barton, Jr.

View On-line

Summer is a great time to relax and reflect. I hope that you’re taking some time to enjoy this season. And for our friends in the southern hemisphere—we hope you’ll cheer for those of us north of the equator as we take a little time away from school or work to enjoy the warm weather.

Several years ago, I wrote about the tendency for the U.S. markets to significantly slow down during the month of August. As we approach that late summer month, I thought it would be interesting to revisit the theme.

Most Augusts are typically a forgettable month in the markets but I remember well the summer of 2011. I sat in a beach house while the U.S. congress ground into gridlock over budget deficit extensions only to have the Standard & Poor’s rating agency downgrade U.S. debt. This happened amid the early phases of the European debt crisis and global markets tumbled massively in just a few days. Included in the hysteria was when the Dow lost more than 650 points - in one single day! No August doldrums that year.

2011 and the real estate crash craziness of 2007, though, seem to be the exceptions rather than the rule as we’ll see in some data.

Summertime, Summertime, Sum, Sum, Summertime…

There are some notable summer vacation clichés about August, like the one about France shutting down for the month and Wall Street grinding to a standstill.

Having worked intimately with a French firm during a technology transfer back in my engineering days, I can say that France doesn’t shut down during August, but things sure do get slow! Many smaller businesses and top officials in government do, in fact, take the month off.

In August of 2003, my family was vacationing in Paris when the infamous heat wave hit France. We spent a week there when the LOWEST daily high was 107 degrees Fahrenheit! That may not seem like much heat to our readers in, say, Arizona — but for Paris, the average daily high temperature in August is 75 degrees! I mention this story because the slow response of the government to the heat wave that killed more than 14,000 people was blamed on the majority of the French health administration who were away on vacation and failed to return in a timely manner to address the crisis.

Does Wall Street Really Slow Down in August?

What about the common perception that Wall Street also has a slow-down in August for similar reasons? To see if this is true, I took two paths to look for an answer. First I talked to a Wall Street veteran to get a firsthand account. And secondly, I looked at the hard numbers to see if they corroborated the cliché.

My best friend and business partner Christopher Castroviejo has over three decades of experience on Wall Street. From a partnership in one of the leading investment banks to running a hedge fund trading desk for many years, Christopher has just about seen and done it all on Wall Street. I asked him about this common perception of a trading slowdown in August.

Christopher said that the “A” team traders and managers do typically head to the Hamptons or the beach for much of August, leaving the “B” team to manage the trading. Those junior traders have strict instructions, both explicit and implicit to maintain the status quo and avoid taking big risks while the ranking staff is away.

“The last thing a senior trader or manager wants to hear is a phone call about a trading problem at 9:30 in the morning after being up with the glitterati until 4:00 a.m.” Enough said.

So the word on the Street is that August is indeed a month of leisure for senior traders. But does the actual market activity support this assumption? To answer that, I looked at volatility as a proxy for market activity. I compared August volatility versus the 12 month average of volatility as measured by Average True Range (ATR). ATR is simply the range (in this case, the monthly range), taking into account gaps. Here’s what the raw data for the last 13 years shows:

August Versus Average Monthly Volatility

Year |

12 Month Ave ATR |

August ATR |

August vs Annual |

2012 |

96.91 |

72.03 |

74.3% |

2011 |

82.47 |

205.84 |

249.6% |

2010 |

86.52 |

89.54 |

103.5% |

2009 |

147.02 |

60.77 |

41.3% |

2008 |

103.28 |

65.70 |

63.6% |

2007 |

68.42 |

133.29 |

194.8% |

2006 |

52.39 |

45.44 |

86.7% |

2005 |

48.89 |

44.79 |

91.6% |

2004 |

49.93 |

48.96 |

98.0% |

2003 |

80.94 |

50.17 |

62.0% |

2002 |

107.60 |

131.56 |

122.9% |

2001 |

126.22 |

101.40 |

80.3% |

2000 |

119.67 |

99.78 |

83.4% |

As you can see, for 9 of the last 13 years, August volatility has been below the monthly average. Only 2002 and the aforementioned years of 2007 and 2011 had Augusts with volatility that was significantly higher-than-average. 2010 stood as the lone case where August had about the same volatility as the rest of the year.

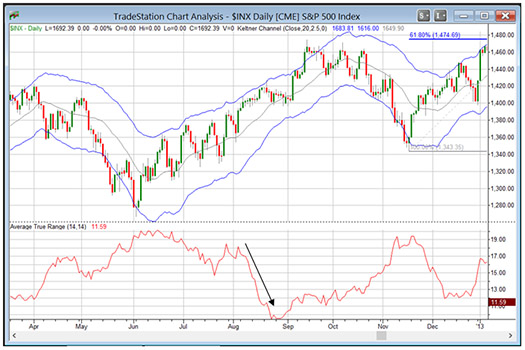

Last year (2012) presented a dreadfully slow August, with only a couple of days breaking that mold. As we see from the chart below, the Average True Range did a disappearing act during the month:

So What?

Should traders and investors take the month of August off? One of Van’s famous “Top Tasks of Trading” is spending time out of the markets, and the summer is a good time to exercise this task! If you do not intend to take the month off, then you don’t have to be completely out of the markets — there are still opportunities, even during August! It would be prudent, however, to demand a bit more from your trade set-ups in what is traditionally a lower volatility month.

Take only the highest quality set-ups in the upcoming month and then relax and refresh. Everyone needs a good break every now and then.

Great Trading,

D. R.

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured guest on both Report on Business TV, and WTOP News Radio in Washington, D.C., and has been a guest on Bloomberg Radio. His articles have appeared on SmartMoney.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Disclaimer

Ken's Class

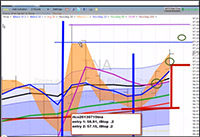

Ken Long presents an extended case study of trades over three days from July 15-17 in this 21-minute video. It turned out that he traded long on the first day, short on the second and then long again on the third. For up moves, he usually bought either TNA (leveraged ETF for the Russell 2000 index) and XIV (the inverse volatility ETF) while he took advantage of down moves with UVXY (the leveraged volatility ETF). His trades were based on regression line crossovers (RLCO), trend moves, and volatility breakouts. He also found a few “special case” trades and provides his reasoning for the entries and exits on those. Ken Long presents an extended case study of trades over three days from July 15-17 in this 21-minute video. It turned out that he traded long on the first day, short on the second and then long again on the third. For up moves, he usually bought either TNA (leveraged ETF for the Russell 2000 index) and XIV (the inverse volatility ETF) while he took advantage of down moves with UVXY (the leveraged volatility ETF). His trades were based on regression line crossovers (RLCO), trend moves, and volatility breakouts. He also found a few “special case” trades and provides his reasoning for the entries and exits on those.

Click here to watch the video

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Click here to take our quick, 6-question survey.

Also, send comments or ask Van a question by clicking here.

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at [email protected].

To stop your subscription, click on the "unsubscribe" link at the bottom left-hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute

Be sure to check us out on Facebook and Twitter!

Back to Top |