Tharp's Thoughts Weekly Newsletter

-

Feature Article:Negative Interest Rates and Deflationary Banking Part One, by Ivan Obolensky

-

Workshops: The Full 2016 Workshop Calendar is Complete Through the End of the Year

-

Trading Tip: Signs that U.S. Markets Trade in Crisis Mode — Even at All Time Highs, by D.R. Barton Jr.

-

New This August!

The Trading in a Bear Market and Down Markets Workshop helps you learn how to think about trading broad bear markets or trading a specific asset class, sector or even single symbol that is in bear mode. For a major bear market, think equities in 2008-2009. For a move limited to a sector move, think oil in 2014-2015. Imagine having had some ways you could have traded those periods effectively. Major bear markets come only once in a while but “lesser” down moves can be found almost any time — including during bull markets. Start using the information from this workshop when you return back home — and also be prepared for the next big bear market.

System Quality Numbersm — A new Workshop in response to long-requested help from our trading clients. Dr. Tharp developed his SQN theories for his book The Definitive Guide to Position Sizing Strategies. Since then, many traders have asked for more information on applying theory for developing effective position sizing strategies that help you meet your objectives—in other words, just HOW to do this. For the first time ever, RJ Hixson will spend two days showing you how to do this through a series of lectures, case studies, individual exercises, and group work.

To register see our workshop schedule below.

Feature Article

Negative Interest Rates and Deflationary Banking

Part One of Two

by Ivan Obolensky

Click here to resolve formatting problems

Many readers have heard of negative interest rates, but few are familiar with them, understand what they mean, and know their ramifications going forward. How is it possible to have negative interest rates on a mortgage, or even a credit card? The bank would pay me money? How is that even possible? The short answer is yes, it’s quite possible. Here’s how and why.

But before we go there, it is necessary to explain some things about money, and why negative interest rates have become a policy option.

Money is a portable storehouse of value. By putting an intermediate step in the barter system, early merchants had a means to store buying power for the future. How did the merchants know that the future buying power they stored would retain its value? The money itself, coinage, was made of precious metals and had an intrinsic value in and of itself. Banks originally were depositories. A merchant received a receipt for his deposited gold, and this receipt could be exchanged for goods and services. The bearer could cash it in at any time.

Some banking houses were financially stronger than others. They had more gold and a better reputation. The latter was important because once a house was trusted, it could create more receipts than the amount of gold on hand and issue them as loans. This is called Fractional Reserve Banking.1 The practice had the potential for abuse. A depositor might demand his deposit back only to find it was not available. This is an old, if not ancient, story.2

The Orazione Trapezitica, written in 393 BCE, records a legal speech by Isocrates (436-338 BCE), one of the foremost Greek orators of his time. In it, he argues for redress on behalf of his client who is seeking the return of deposits from Passio, an Athenian Banker, who refused, for whatever reason, to return them.3

In spite of the risk of abuse, Fractional Reserve Banking has its pluses. It allows loans to be made to those who need funds to start businesses, which create additional economic value in the form of employment and future production of goods and services. Without the initial funding, the potential positive economic benefit would never be realized.

Money, therefore, represents many things: physical goods, labor, as well as the amount of work necessary to make something. It is also a storehouse of future value in that it has the potential to create and purchase goods in the future. It has buying power.

Beyond what it represents, money is also a commodity that can be bought and sold like any other. When one gets a loan, one is buying money. When one is a lender one is selling money. If you are buying flour, it is so much per pound. When you buy money, the price you pay is so much interest per thousand expressed as an annual percentage rate.

Money is cheap when interest rates are low and expensive when interest rates are high. Cheap money in the past has usually led to economic growth and inflation.

Inflation is defined as too much money representing too few goods, and deflation as too little money representing too many goods. In an inflation, prices of things go up. In a deflation, the prices of goods fall.

Whether prices go up or down depends on the economic forces that are dominant.

If money is plentiful and inflation is widespread, market participants, including consumers and corporations, go on buying binges. It becomes economically wise to move money into physical things such as cars, gold, and real estate as fast as possible. The longer you hold onto money, the less it can buy. The more physical things you own, the more valuable they become. In such a system, money moves rapidly from consumer to merchant to wholesaler, and around and round. Debt is of benefit because not only does one buy things that are rising in price and retaining their value, but the money purchased in the form of loans is paid back with funds that are less valuable based on their buying power. This is a powerful incentive to spend.

Controlling this tendency is the province of central banks such as the US Federal Reserve.

Central banks have a mandate to maintain economic stability. One of the tools for that purpose is setting the level of short-term interest rates. By raising rates, money becomes expensive, economic activity is slowed, and inflation is halted. If the economy slows too much, interest rates are lowered to make money easily available, and the economy speeds up.

The last several decades can be characterized as a long period of inflation. Inflation promotes spending and thus consumerism.

Consumerism has been one of the most prevalent paradigms in Western and developing economies for well over thirty years. The attitude flourished during the long-term inflationary environment that started in the 1960s. During inflationary times, thrift, savings, and fiscal responsibility actually work against the individual, while conspicuous consumption and excessive debt are rewarded.

Economies, contrary to much academic teaching, are cyclical. Growth is neither constant nor is it guaranteed. It occurs in cycles. Deflations have followed periods of inflation over and over until the last century. The 1930s marked the last time the world has seen a prolonged deflation. Much of the praise for this long inflationary stretch has been given to central bank policies and actions that steered a middle course between economies that are too hot or too subdued, until now.

Today, deflation is much more pervasive, and deflations are very different economic environments from inflationary ones.

Operating in a deflation requires that you put off a purchase for as long as possible since whatever it is will be cheaper in the future. Immediate gratification becomes not only unwise but a distinct liability. Cash money earns interest sitting in the wallet because it will buy more and more over time.

Notice this is the opposite mindset to consumerism.

Deflation is not new. It has happened many times throughout history. Why is this time different?

In the past, economies routinely moved into inflationary credit bubbles that led to excessive spending, unwise investment, and overextended borrowers. (The US during the 1860s and 1930s.) As these economies reached their apex and started to contract, debtors could no longer support their debt and defaults became prevalent. Loans are potential assets to a bank since they generate income in the form of interest payments. When there is a default, the asset value of the loan is reduced, often to zero. Banks close (they become bankrupt) just like the depositories and banking houses of long ago. Bankers stop lending. Money becomes scarce, prices drop (deflation), and the economy grinds to a crawl until the bad loans are written off and a new cash infusion is provided. After a time, with the start once again of easy credit, the cycle repeats.4

In the past, deflationary cycles were a fact of life. There were no central banks. Since their inception at the start of the 20th century, there has been only one deflationary period of significance: The Great Depression, and central banks did not handle it well. Nothing worked over the long term. WWII is said to have pulled the US out of the depression more than any particular policy or action taken alone or altogether.

Being aware of this, current central bank policy is to prevent a deflationary economic slowdown by any means possible with the intention of recreating an inflationary environment while avoiding the defaults of past cycles.

Pushing money into the financial system to provide liquidity, providing as much easy money as possible by lowering interest rates to minimal levels, and preventing significant defaults are actions that were not taken in the 1930s. Banks closed in record numbers during that time and defaults were common, including sovereign debt issued by governments throughout the world.

Today the world’s financial and banking structure is very different from over a century ago. There are safeguards in place such as deposit insurance, but global financial institutions are significantly more interconnected. In the 30s, banks were isolated businesses, but not so today. A large loan default in one bank could lead to a cascade of counterparty defaults in others, precipitating a worldwide banking crisis. Although the effects of such a collapse are impossible to know with certainty, the Global Financial Crisis (GFC) of 2008 was an indication of how easily it could happen. The US was days away, in the autumn of 2008, from no available cash for payrolls. What would have happened had a large segment of the US population not been paid is a nightmare scenario that nobody holding economic responsibility dares risk finding out. Thus, providing liquidity by any means and avoiding major defaults have become the two overarching central bank policies because, in essence, there are no alternatives.

To add to central banks’ difficulties, much of their ammunition in the form of room to lower rates (rates are already close to zero), swapping bad debt for good debt, and cash infusions, has already been used up with limited success. The crisis, although eight years past, is to some extent, still with us.

After several rounds of the above, widespread inflation has failed to appear. Rather, the results have been a disparity of wealth and an asymmetric US economy that shows inflationary pressures occurring in only certain segments such as housing, healthcare, education, and stock market valuations, while deflationary pressure remains persistent in others such as commodities and wages.

In part two of this article next week, we will learn the reasons why widespread inflation has failed to appear in the United States. Ivan will explore a lesson learned from Japan and what we might learn about that country’s negative interest rates and deflationary banking experience.

Copyright © 2016 Ivan Obolensky http://www.dynamicdoingness.com

Ivan is a member of Dr. Tharp's Super Trader Program. We look forward to publishing more of his insightful articles.

- Tamny, J. (2012) Ron Paul, Fractional Reserve Banking, and the Money Multiplier Myth, Forbes. Retrieved May 5, 2016 from http://www.forbes.com/sites/johntamny/2012/07/29/ron-paul-fractional-reserve-banking-and-the-money-multiplier-myth/#76aaba0b6704.

- Gascoigne, B. (2001) History of Banking, History of the World. Retrieved May 5, 2016 from http://www.historyworld.net/wrldhis/PlainTextHistories.asp?groupid=2450&HistoryID=ac19>rack=pthc.

- Huerta de Soto, J. (2006) Money, Bank Credit, and Economic Cycles. Retrieved May 5, 2016 from https://mises.org/sites/default/files/Money_Bank_Credit_and_Economic_Cycles_De%20Soto.pdf.

- Garrison, R. (2002) Business Cycles: Austrian Approach. Retrieved May 5, 2016 from http://www.auburn.edu/~garriro/c6abc.htm

Super Trader

We Basically Just Reduced the Price of the Super Trader Program By 25% And You Have Till The End of July to Get The Old Pricing

Interested traders have until July 31st to take advantage of a huge reduction in the price of the Super Trader program. In the old Super Trader program, students paid for three years of Super Trader 1 upfront, and then paid for at least one more year when they started Super Trader 2. Thus, the minimum cost of the program was $66,750. Now, however, students can finish the program in three years for a total investment of only $50,250. For motivated and committed traders looking to transform themselves and their trading, that’s a huge effective discount of $16,750.

If you have been considering joining the program but have been putting off your decision, you have until the end of July to seize your opportunity to act and save big. On August 1st, the price of the program will increase by several thousand dollars (but the ability to finish in three years will still be available.) The longer you wait, the higher the cost - in 2017, we will raise the price of the program tuition to $20,000 per year.

I recently wrote an article on the change in the structure of the program which you can read here.

If you'd like to see the most updated information on the new Super Trader structure click here to view it online, or click here to download a PDF of the new program overview.

Workshops

Combo Discounts available for all back-to-back workshops!

See our workshop page for details.

Trading Tip

Signs that U.S. Markets Trade in Crisis Mode — Even at All Time Highs

by D. R. Barton, Jr.

Click here to resolve formatting problems

Brexit . . . remember that little vote on the island kingdom 20 calendar days ago? That price drop is now an event distant in the rear view mirror — according to the market. The S&P 500 and the Dow Jones Industrial Averages just made new all-time highs.

Meanwhile, the more volatile Nasdaq and Russell 2000 indexes are many percent off of their highs. That disparity tells a big part of the problem. I’ve written many times before about the concept of “risk on” assets vs. “risk off” assets. With the risk-on Nasdaq and Russell short of their all-time highs, this current rally is rather upside down - as is 2016’s market action in general.

This week we’ll look at one sign that in spite of the all-time highs, this market is in crisis mode. (Next week, we’ll look at a second sign.)

What is Crisis Mode?

First, let’s define market “crisis mode”. It’s pretty simple — some analysts use this term for how the markets acted (and reacted) after the end of the Great Recession (2008 – 2009). Many observed a structural change in the way markets behaved after the crisis versus before:

- Abrupt declines of greater than 5% (but less than 10%) were followed by a quick snapback; this strategy of buying all pullbacks was aided and abetted by the perception that central banks would continue to provide a safety net under the markets.

- Correlation between geographic regions and asset classes grew to a very large extent and gave rise to risk-on (assets that move strongly up when markets are in a bull phase) and risk-off (assets that do better in bear phases).

We’ve seen another instance of a sharp decline (the two days after the Brexit vote) followed by a quick snapback.

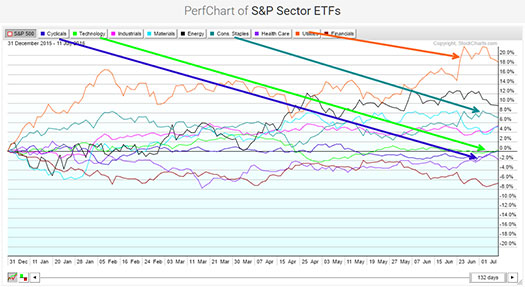

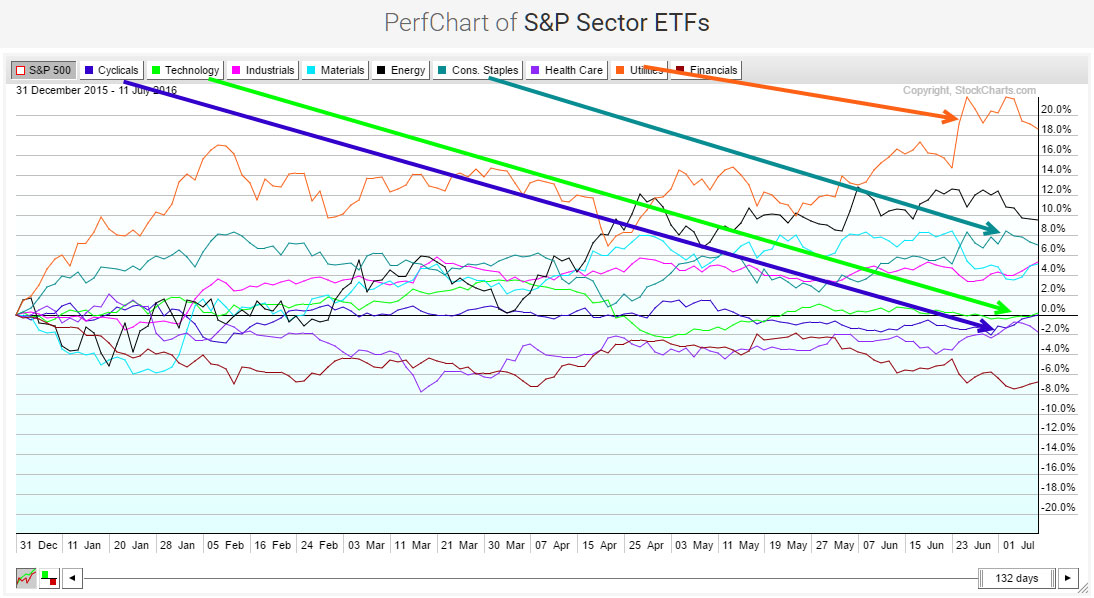

View larger

And now let’s look at the first of two additional signs that we’re still in crisis mode trading.

Sign #1: Defensive Sectors Lead the Way

In the risk-on versus risk-off paradigm, certain sectors have classically been associated with one side or the other. One of the classic pairs is the Consumer Staples sector (XLP) vs. Consumer Discretionary (XLY). You can see how these two sectors contrast by looking at their top holdings:

XLP’s Top Holdings:

- Everyday consumables — beverages soap, toothpaste, paper goods, etc.: Proctor & Gamble (index weight: #1), Coca-Cola (#2), PesiCo (#8) and Colgate-Palmolive (#10)

- Tobacco: Philip Morris (#3) and Altria (#4)

- Discount Retail & Pharmacies: Walmart (#5), CVS (#6) and Walgreens (#9)

XLY’s Top Holdings:

- Discretionary Retail: Amazon (#1), Home Depot (#2), and Lowes (#8)

- Travel & Entertainment: Comcast (#3), Disney (#4), Priceline (#9) and Time Warner (#10)

- Restaurants / Coffee: McDonalds (#5), and Starbucks (#6)

- Recreational Wear: Nike (#7)

The idea why discretionary is the risk-on sector is pretty clear — when times are good, we spend more on leisure and discretionary retail. When times are not so good, money becomes tight and the last things to cut back on are staples and therefore this sector is the traditional risk-off choice.

Let’s see where these sectors are in terms of year-to-date performance. This is what Stockchart.com calls a performance chart or a percentage gain/loss chart of the nine sectors classified by Standard and Poor’s. Note that stockcharts.com uses the term “Cyclicals” instead of “Consumer Discretionary” for XLY:

View larger

You can see on the chart that risk-off consumer staples have significantly outperformed their risk-on sibling — discretionary (cyclical).

In addition, I highlighted another risk-on/risk-off sectors pair in the chart: the traditional risk-on technology sector (bright green) and the very defensive, risk-off utilities sector (orange). In a flip flop of what you’d expect to find in a market making new all-time highs, we have technology in the bottom half of performers this year and another defensive sector (utilities) leading the way!

It’s almost as if investors and traders are saying, “Ok, we’ll buy because people are still jumping in at every dip, but we’re going to buy cautiously…”

Sign #2

Next week, we’ll look at second sign the market is in crisis mode - some enlightening market correlation numbers from one of the world’s biggest hedge funds, Renaissance Capital. We’ll see if we can draw some useful conclusions from that data.

Please send your thoughts and comments to drbarton “at” vantharp.com — I always appreciate hearing from you!

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured analyst on Fox Business’ Varney & Co. TV show (catch him most Thursdays between 12:30 and 12:45), on Bloomberg Radio Taking Stock and MarketWatch’s Money Life Show. He is also a frequent guest analyst on CNBC’s Closing Bell, WTOP News Radio in Washington, D.C., and has been a guest on China Central Television — America and Canada’s Business News Network. His articles have appeared on SmartMoney.com MarketWatch.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Free Book

FREE Book!

TRADING BEYOND THE MATRIX

The Red Pill for Traders and Investors

We pay for the book, you pay for shipping.

ALL YOU HAVE TO DO IS CLICK HERE!

Eleven traders tell their stories about transforming their trading results and lives, in this 400 plus page book.

Below is a brief video on how powerful this book is to traders.

Swing Trading Systems E-Learning Course

Ken Long's systematic approach to swing trading with 5 distinct trading systems. This course has over 10 hours of instruction with significant follow-along documents included for students to download.

Review the videos as many times, and as often as you like, for one full year. Plus, you receive a bonus workshop at no extra charge—Dr. Van Tharp's Tharp Think Essentials!

If you are interested in both this video home study program (featuring mechanical, rule-based systems) and our new Advanced Adaptive Swing workshop (adaptive trading systems have rules and rule parameters that adjust to market conditions and price conditions rather than remaining constant) you benefit by buying both at the same time.

When you register for the workshop you can get a 22% discount on this home study.

The home study is not required to attend the workshop, however, an understanding of the systems in the the video home study may help a less experienced trader better understand the more advanced trading style which will be presented in the workshop. The systems, however, are totally different and the Advanced Adaptive Systems Workshop does not build upon the systems in the home study.

You can complete this course at your own pace, from the comfort of your own home or office, and access the materials as many times as you wish during your 1-year subscription period.

Take a look at this video from Ken to learn more about this course.

We have extensive information about the Swing Trading System e-learning course, including how to purchase...click the link below!

Learn More About The Swing E-Learning Course...

Matrix Contest

Enter the Matrix Contest Enter the Matrix Contest

for a chance to win a free workshop!

We want to hear about the one most profound insight that you got from reading Van's new book, Trading Beyond the Matrix, and how it has impacted your life. If you would like to enter, send an email to [email protected].

If you haven't purchased Trading Beyond the Matrix yet, click here.

For more information about the contest, click here.

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Send comments or ask Van a question by clicking here.

Also, Click here to take our quick, 6-question survey.

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at [email protected].

To stop your subscription, click on the "unsubscribe" link at the bottom left—hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

Call us at: 800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute and the International Institute of Trading Mastery, Inc.

Be sure to check us out on Facebook and Twitter!

Van Tharp Home • Products • Workshops • Back Issues • Contact • About Van Tharp • Site Map ———————

Back to Top |

{kind=link}

{kind=link}