Tharp's Thoughts Weekly Newsletter

-

Feature Article:Negative Interest Rates and Deflationary Banking Part Two, by Ivan Obolensky

-

Workshops: Forex Live Trading Has Been Expanded

-

Trading Tip: Signs that U.S. Markets Trade in Crisis Mode –

Even at All Time Highs: Part 2, by D.R. Barton Jr.

-

New This August!

The Trading in a Bear Market and Down Markets Workshop helps you learn how to think about trading broad bear markets or trading a specific asset class, sector or even single symbol that is in bear mode. For a major bear market, think equities in 2008-2009. For a move limited to a sector move, think oil in 2014-2015. Imagine having had some ways you could have traded those periods effectively. Major bear markets come only once in a while but “lesser” down moves can be found almost any time — including during bull markets. Start using the information from this workshop when you return back home — and also be prepared for the next big bear market. Click here to read how Bear markets present traders with a unique set of opportunities.

System Quality Numbersm — A new Workshop in response to long-requested help from our trading clients. Dr. Tharp developed his SQN theories for his book The Definitive Guide to Position Sizing Strategies. Since then, many traders have asked for more information on applying theory for developing effective position sizing strategies that help you meet your objectives — in other words, just HOW to do this. For the first time ever, RJ Hixson will spend two days showing you how to do this through a series of lectures, case studies, individual exercises, and group work.

For an overview of this workshop watch our short 3 minute video.

To register see our workshop schedule below.

Feature Article

Negative Interest Rates and Deflationary Banking

Part Two

by Ivan Obolensky

Click here to resolve formatting problems

Editor's Note: Last week in Part One of this article, Super Trader student Ivan Obolensky introduced us to the concept of negative interest rates by giving us an historial overview of inflation and deflation.

Ivan explained that “the current central bank policy is to prevent a deflationary economic slowdown by any means possible with the intention of recreating an inflationary environment while avoiding the defaults of past cycles.” He went on to explain that after several rounds of precautionary measures, widespread inflation has failed to appear and that instead, “the results have been a disparity of wealth and an asymmetric US economy that shows inflationary pressures occurring in only certain segments such as housing, healthcare, education, and stock market valuations, while deflationary pressure remains persistent in others such as commodities and wages.”

We pick up this week with reasons why widespread inflation has failed to appear. Besides the cyclical deflation that happens during a typical credit cycle, there are several long-term deflationary forces at work today that the central banks must contend with that are making their job much more difficult.

Technology: Technology will always create deflation since, by its very nature, it makes devices, manufacturing, and distribution more efficient and less expensive.

Demographic aging in developed economies: Populations of the developed economies are on average getting older and tend to spend more on health care and services than goods, driving down their demand.5

Globalization: Interconnectivity and free trade has created deflationary pressures in the form of lower costs of manufacturing as well as compensation competition across all segments of society. Free trade agreements have taken down barriers that previously allowed developed countries to insulate themselves from competition. Japan is a notable example. Once the walls came down, prices of labor services and goods dropped and are still doing so after more than twenty-five years.

The Internet: The greatest disruptions to tariff and economic barriers have come from the internet. By putting millions of potential workers, corporations, products, and services on an equal footing, costs have fallen while providers’ and manufacturers’ ability to increase prices has been curtailed by competition.

Productivity: Productivity has been dropping in developed countries, particularly in the United States. On an individual basis, one of the reasons cited has been the increasing amounts of production time wasted on social media as the need for labor intensiveness decreases.6 At the same time, AI, computer controlled operations, algorithms, and robotics require less need for direct human action and supervision. Money is able to buy more product for the same amount of expensive human labor which is being replaced by automation as quickly as possible. This is deflationary and is a trend likely to continue.

Given these global deflationary themes, policy-makers must create inflation in spite of them.

Japan was the first developed country to have to deal with a long-term deflation. It is still ongoing with no end in sight. They tried what is known as Helicopter Money, simply dumping cash into the pockets of citizens in the billions of dollars. It disappeared. Where did it go? Most of it went into freezers. In the 1990s, trading desks referred to Japan as the Freezer Economy. Recall that the mindset for a deflation is significantly different from that of inflation. The Japanese had already experienced years of deflation and simply took the cash and literally stored it in their freezers often in blocks of ice. Sitting there it earned phantom interest because with every month, the cash could buy more things.

Japan was also the first to implement negative interest rates and have for some time. Short-term government bonds were sold with a built-in premium that guaranteed that the holder would lose money, but doing this was far smarter than one might think. Japanese banks were not trusted and because the deflation rate of say 3% was greater than the guaranteed loss sustained holding the government bond to maturity (1.5%), the holder actually made money in terms of buying power.

Since then, the Japanese government has gone heavily into debt (237% of Gross Domestic Production7). It also purchased most of the extant Japanese corporate bonds and is one of the largest holders of Japanese equities in an effort to support their markets. It is likely other central banks have observed the path the Japanese have taken and will reluctantly follow their example.

With most of the world’s interest rates near zero, negative interest rates are the next logical step in the search for economic stimulus by policy makers.

Negative interest rates will mean that holders of reserves rather than earning interest will be charged interest. The logic behind this policy is that savers, including corporations, will spend in the real economy rather than save. But policy makers have also learned from the Japanese foray into Helicopter money. Money pumped directly into the pockets of citizens will disappear into freezers and under mattresses.

Is it any wonder that the war on cash has begun under the pretext of denying criminals and terrorists access to funding?

Taking cash out of the bank and hiding it has been the recourse of citizens when confronted with a financial crisis as long ago as 400 BCE, if not before. Federal Deposit Insurance was created to alleviate depositors’ tendency to do just that after the banking panics of the Great Depression. Recently, the ECB announced that the 500-Euro note would no longer be printed as of 20188. Also, several noteworthy economists have announced that cash should be gotten rid of as it is unnecessary in a digital age.9 This is not coincidence.

But how can such a policy be implemented?

Negative interest rates mean that wherever interest is paid, the flow is reversed. In a savings account, the holder would be charged a monthly fee, or negative interest. Wherever interest must be paid (credit card debt, mortgage debt) by the debtor, the lender pays it to the debtor instead.

Think about that. If this seems confusing think about the Japanese and their freezers. It’s not about the money. It’s about what the money can buy.

Example: Suppose you are an apple merchant; you want to sell your apples for a higher amount than what you paid for them.

If there are few apples, you purchase apples at high prices and then add a markup. Your customers have to simply pay more.

What happens if you bought apples when they were really cheap, preserved them in some way, and then sold them at a later time when the price of apples was high? You would make a lot more money.

If you bought the apples when they were high, preserved them, and then had to sell them in a marketplace where apples were cheap, you would lose a lot of money.

Simple so far. Recall that money is a commodity just like the apples.

Let’s suppose you decide to lend out your apples rather than sell them. The market is cheap. You lend ten apples to a customer for a year, but you are a kind soul and say, “Look it’s possible that the price of apples could go up, so I tell you what, since you are a good person, pay me only six apples next year. How about that?”

The customer agrees. Such a deal! A year later the price of apples has tripled, and the customer comes back and gives you six apples. You paid a dollar an apple, but apples are now three dollars each. The customer pays you six apples now worth 18 dollars.

The apples you received were much more expensive than the ones the customer borrowed the year before.

In this, you have the concept of how banks could make money with negative interest rates.

Suppose I borrow 1,000 dollars and a bank says, “Thank you for borrowing that money and as a special reward, we will pay you 120 dollars, or ten dollars a month, credited to your checking account.”

I agree. Such a deal! A year later I pay back the 1,000 dollars, only I notice the thousand dollars I paid can now buy twice as much as it did before. I just paid the bank $1,000 now worth $2,000 in terms of buying power. All told, I borrowed 880 dollars if I deduct the interest the bank paid me. The bank, on the other hand, paid out $1,120 and received back $1,000, which because of deflation is now worth $2,000 in terms of buying power. In real terms, the bank profited by $880.

This works with any mortgage just as easily, only the numbers are larger.

Such seemingly bizarre policies are not so bizarre after all but are still a holding action. The real question before central banks is: how to ultimately avoid the default consequences that normally occur during a credit cycle while still preserving the banking system from vaporizing?

There are solutions. Some have already been tried.

The bailout (government stepping in with taxpayer money) was one method and was given full rein in the months and years following 2008 with limited success.

The other is the bail-in.10 This was done in Cyprus and Greece relatively recently. Depositors over a certain amount simply forfeited a portion (30%) of their savings.11 This also worked to some degree; however, many depositors had the foresight to cash in their deposits via ATMs before the bail-in occurred. Others transferred their funds to accounts in other countries.

For a bail-in to work, it is necessary for depositors to keep their money within the system, which means a fully digital economy. The more funds on hand the less the forfeiture the depositors have to endure.

Whether this will actually occur is unknown, but with no alternative readily available, it might.

At some point, whether in the far distant future or closer still, the question of how to keep the financial system going must be answered and actions taken.

Welcome to the world of deflationary banking. It might not happen, but then again it might.

Copyright © 2016 Ivan Obolensky http://www.dynamicdoingness.com

Ivan is a member of Dr. Tharp's Super Trader Program. We look forward to publishing more of his insightful articles.

- Mauldin, J. (2016) 6 Charts that show the Global Demographic Crisis is Unfolding, Forbes. Retrieved May 5, 2016 from http://www.forbes.com/sites/johnmauldin/2016/05/02/6-charts-that-show-the-global-demographic-crisis-is-unfolding/#4225bc475e26.

- A. (2016) America’s Plunging Worker Productivity Explained (in 1 Depressing Chart) Zero Hedge. Retrieved May 5, 2016 from http://www.zerohedge.com/news/2016-05-02/americas-plunging-worker-productivity-explained-1-depressing-chart.

- Ewing, J. (2016) Europe to remove the 500-Euro Bill, the ‘Bin Laden’ Bank Note Criminals Love, The New York Times. Retrieved May 5, 2016 from http://www.nytimes.com/2016/05/05/business/international/ecb-to-remove-500-bill-the-bin-laden-bank-note-criminals.html?_r=0.

- Elmore, Kirkwood, Chehabi, Evans (2013) The spiraling Cost of Debt, A Study on the Impact of Debt on GDP Growth and Long Term Interest Rates. Retrieved May 5, 2016 from http://glendontodd.com/wp-content/uploads/2014/10/2013-Marco-Project-Debt-to-GDP.pdf.

- A. (2016) Larry Summers Launches the War on Paper Money: “It’s Time To Kill the $100 Bill”, Zero Hedge. Retrieved May 5, 2016 from http://www.zerohedge.com/news/2016-02-16/larry-summers-launches-war-us-paper-money-its-time-kill-100-bill.

- Zhou, Rutledge, Bossu, Dobler, Jassuad, Moore (2012) From Bail-out to Bail-in: Mandatory Debt Restructuring of Systemic Financial Institutions, International Monetary Fund. Retrieved May 5, 2016 from https://www.imf.org/external/pubs/ft/sdn/2012/sdn1203.pdf

- Osbourne, H., Moulds, J. (2013) Cyprus Bailout deal: at a glance, The Guardian. Retrieved May 5, 2016 from https://www.theguardian.com/business/2013/mar/25/cyprus-bailout-deal-at-a-glance.

Super Trader

We Basically Just Reduced the Price of the Super Trader Program By 25% And You Have Until Next Friday to Get The Old Pricing

Interested traders have until July 31st to take advantage of a huge reduction in the price of the Super Trader program. In the old Super Trader program, students paid for three years of Super Trader 1 upfront, and then paid for at least one more year when they started Super Trader 2. Thus, the minimum cost of the program was $66,750. Now, however, students can finish the program in three years for a total investment of only $50,250. For motivated and committed traders looking to transform themselves and their trading, that’s a huge effective discount of $16,750.

If you have been considering joining the program but have been putting off your decision, you have until the end of July to seize your opportunity to act and save big. On August 1st, the price of the program will increase by several thousand dollars (but the ability to finish in three years will still be available.) The longer you wait, the higher the cost - in 2017, we will raise the price of the program tuition to $20,000 per year.

I recently wrote an article on the change in the structure of the program which you can read here.

If you'd like to see the most updated information on the new Super Trader structure click here to view it online, or click here to download a PDF of the new program overview.

Workshops

Combo Discounts available for all back-to-back workshops!

See our workshop page for details.

Trading Tip

Signs that U.S. Markets Trade in Crisis Mode –

Even at All Time Highs: Part 2

by D. R. Barton, Jr.

Click here to resolve formatting problems

In the first part of this series last week, we talked about a market that keeps pushing higher but that also has the underlying characteristics of a market in crisis. We looked at the first sign that the market is in crisis and this week, we’ll dive into a second sign.

Sign #1: Defensive Sectors Leading

We revisited the concept of “risk on” assets vs. “risk off” assets and one week later, we still see the broader S&P 500 and blue chip DOW stocks continuing to lead this rally. Meanwhile, the “risk on” Nasdaq and the Russell asset teams continue to lag during the big push up.

We also saw that traditionally, the defensive (“risk off”) sectors in utilities and consumer staples are the leading gainers in 2016. For a quick read of that article and the charts showing this you can click here.

This week I want to highlight some work on market correlation numbers from Renaissance Capital, but first, a quick reminder.

What is Crisis Mode?

Let’s revisit a definition for “crisis mode” trading action. It’s pretty simple — some analysts use this term to describe how the markets acted (and reacted) after the end of the Great Recession (2008 – 2009). Many observed a structural change in the way markets behaved after the crisis versus before:

- Abrupt declines of greater than 5% (but less than 10%) were followed by quick snapback; this strategy of buying all pullbacks was aided and abetted by the perception that central banks would continue to provide a safety net under the markets

- Correlation between geographic regions and asset classes grew to a very large extent and gave rise to “risk on” (assets that move strongly up when markets are in a bull phase) and “risk off” (assets that do better in bear phases).

Sign #2: Correlations Remain Sky High

Last week Neil Dutta at Renaissance Macro hedge fund sent out to clients a research piece about the high correlations between asset classes — which you would traditionally expect to be uncorrelated.

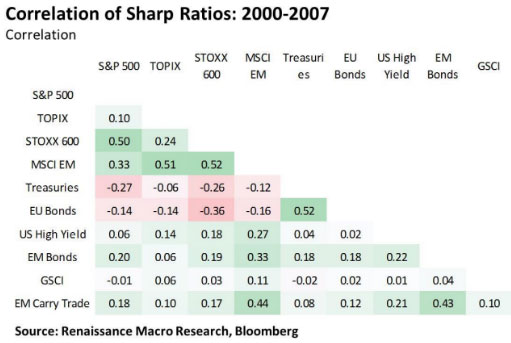

Here’s the table that shows how low the correlations used to be even through the years leading up to the start of the global financial crisis in 2007:

After the Great Recession, these correlations went quite high, a common occurrence for corrections but — then those correlations stayed high for several years — which is very uncommon. Back in 2012, I wrote a series of articles about this very phenomenon where we dug into how markets had traded rather independently before the 2007 – 2008 crash but after the Great Recession, how they traded very similarly (or in a correlated way).

Dutta notes that we are still in the same boat. In his words:

"The global financial crisis started almost 10-years ago and while that may be a distant memory for some, it left a lasting imprint on the global economy. For financial markets, the behavior of asset prices continues to exhibit crisis rather than pre-crisis characteristics.”

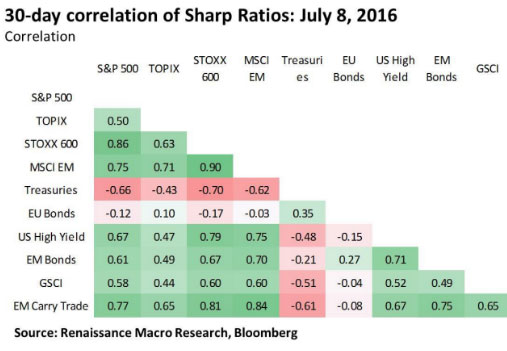

To his point, compare the correlations of those same markets in mid-2016:

Dutta continues:

“The one implication we would like to point is that because of the high correlations, market volatility in one country is more likely to be transferred to another and more quickly."

Next week, we’ll look draw some conclusions and offer some guidance for dealing with this crisis mode market — that keeps making new all-time highs.

Please send your thoughts and comments to drbarton “at” vantharp.com — I always appreciate hearing from you!

Great Trading,

D. R.

About the Author: A passion for the systematic approach to the markets and lifelong love of teaching and learning have propelled D.R. Barton, Jr. to the top of the investment and trading arena. He is a regularly featured analyst on Fox Business’ Varney & Co. TV show (catch him most Thursdays between 12:30 and 12:45), on Bloomberg Radio Taking Stock and MarketWatch’s Money Life Show. He is also a frequent guest analyst on CNBC’s Closing Bell, WTOP News Radio in Washington, D.C., and has been a guest on China Central Television — America and Canada’s Business News Network. His articles have appeared on SmartMoney.com MarketWatch.com and Financial Advisor magazine. You may contact D.R. at "drbarton" at "vantharp.com".

Free Book

FREE Book!

TRADING BEYOND THE MATRIX

The Red Pill for Traders and Investors

We pay for the book, you pay for shipping.

ALL YOU HAVE TO DO IS CLICK HERE!

Eleven traders tell their stories about transforming their trading results and lives, in this 400 plus page book.

Below is a brief video on how powerful this book is to traders.

Swing Trading Systems E-Learning Course

Ken Long's systematic approach to swing trading with 5 distinct trading systems. This course has over 10 hours of instruction with significant follow-along documents included for students to download.

Review the videos as many times, and as often as you like, for one full year. Plus, you receive a bonus workshop at no extra charge—Dr. Van Tharp's Tharp Think Essentials!

If you are interested in both this video home study program (featuring mechanical, rule-based systems) and our new Advanced Adaptive Swing workshop (adaptive trading systems have rules and rule parameters that adjust to market conditions and price conditions rather than remaining constant) you benefit by buying both at the same time.

When you register for the workshop you can get a 22% discount on this home study.

The home study is not required to attend the workshop, however, an understanding of the systems in the the video home study may help a less experienced trader better understand the more advanced trading style which will be presented in the workshop. The systems, however, are totally different and the Advanced Adaptive Systems Workshop does not build upon the systems in the home study.

You can complete this course at your own pace, from the comfort of your own home or office, and access the materials as many times as you wish during your 1-year subscription period.

Take a look at this video from Ken to learn more about this course.

We have extensive information about the Swing Trading System e-learning course, including how to purchase...click the link below!

Learn More About The Swing E-Learning Course...

Matrix Contest

Enter the Matrix Contest Enter the Matrix Contest

for a chance to win a free workshop!

We want to hear about the one most profound insight that you got from reading Van's new book, Trading Beyond the Matrix, and how it has impacted your life. If you would like to enter, send an email to [email protected].

If you haven't purchased Trading Beyond the Matrix yet, click here.

For more information about the contest, click here.

Ask Van...

Everything we do here at the Van Tharp Institute is focused on helping you improve as a trader and investor. Consequently, we love to get your feedback, both positive and negative!

Send comments or ask Van a question by clicking here.

Also, Click here to take our quick, 6-question survey.

Back to Top

Contact Us

Email us at [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

To change your e-mail Address, e-mail us at [email protected].

To stop your subscription, click on the "unsubscribe" link at the bottom left—hand corner of this email.

How are we doing? Give us your feedback! Click here to take our quick survey.

Call us at: 800-385-4486 * 919-466-0043 * Fax 919-466-0408

SQN® and the System Quality Number® are registered trademarks of the Van Tharp Institute and the International Institute of Trading Mastery, Inc.

Be sure to check us out on Facebook and Twitter!

Van Tharp Home • Products • Workshops • Back Issues • Contact • About Van Tharp • Site Map ———————

Back to Top |