|

Trading Education

Van Tharp's Peak Performance Home Study Course People do not trade the market. They trade their beliefs about the market.

These are just a few of the benefits of the Peak Performance Home Study Program. Click Here to Learn More About the Course...

|

Tharp�s Thoughts

Market Update from April 28, 2006

1-2-3 Model Still in Red Light Mode

By

Van K. Tharp

Look for these monthly updates in the first issue of each month. This allows us to get the closing month data. In these updates, we�ll be covering each of the major models mentioned in the Safe Strategies book: 1) the 1-2-3 stock market model; 2) the five week status on each of the major stock U.S. stock market indices; 3) our new four star inflation-deflation model; and we�ll be 4) tracking the dollar.

Part I: Market Commentary.

The down season for the stock market is typically May through November. By May most people have deposited their retirement accounts into their plans. That means that the mutual funds have less money to add to the market and the market tends to go down. We�ve now had 16 straight interest rate increases. Inflation, according to the latest pronouncements from the Federal Reserve, doesn�t seem to be under control, so expect more rate increases. Remember what happened with interest rate increases in 1999.

Perhaps this year will continue with basically flat performance, but I actually think the chances are favorable for 2006 to be a major down year. However, even if that occurs, there will be excellent ETFs in which to park your money (most foreign stocks are doing well) and many �commodity� stocks, which should do well. But 2006 is definitely not a great year to have your money in mutual funds.

Part II: The 1-2-3 Stock Market Model IS IN RED LIGHT MODE.

Let�s look at what the market has done over the last five weeks and compare that with where the averages were December 31st 2005. This is given in the next table. Incidentally, this data is calculated by hand based upon last Friday�s close (i.e., April 28 , 2006), so there is always a possibility of human error in our numbers.

| Weekly Changes in the Major Stock Market Indices | ||||||

|

Date Week Ending |

DOW

30 |

Change |

SP500 |

Change |

NAS 100 (NDX) |

Change |

| 12/31/04 | 10,783.01 | 1211.12 |

1621.12 |

|||

| 12/30/05 |

10,717.50 | -0.6 | 1248.29 |

+3.1 | 1645.20 |

+1.5% |

| 3/31/06 |

11,109.32 |

-1.5% | 1294.87 |

-0.6% | 1703.66 |

+1.5% |

| 4/7/06 |

11,120.04 | +0.1% | 1295.50 |

+0.0% | 1723.03 |

+1.1% |

| 4/14/06 |

11,137.65 | +0.2% | 1289.12 |

-0.5% | 1712.07 |

-0.6% |

| 4/21/06 |

11,347.45 | +0.1% | 1311.28 |

+0.2% | 1709.02 |

-0.2% |

| 4/28/06 | 11,367.14 | +0.2% | 1310.61 | -0.0% | 1700.71 | -0.5% |

I show weekly changes in the major averages because they provide a good contrast to me from the changes I used to see during the great secular bull market that lasted until 2000. During that period, weekly changes in the DOW and S&P 500 averaged about 2-2.5% per week. Notice that current monthly changes are not that big. The Nasdaq 100 could easily show weekly changes as big as 5%. Contrast that with the weekly change in April that was down 3.05 points or 0.18%. There is just not much change in the market these days and that�s been the case since the major downturn stopped in 2002.

Efficient stocks. What�s the market telling me in terms of efficiency? Here, the data is very interesting. I now have a proprietary indicator of the entire market � its efficiency. What percentage of the stocks that I screen show positive efficiency? What percentage of the stocks that I screen show negative efficiency? I�ve only been doing this for about six months so I don�t have much historical data. However, the market continues to be very strong by this measure. As of Monday night (May 1st), 68.2%% of the stocks in my database (over 4000 stocks) show positive efficiency, while only 31.8% of the market is negative. This is a drop of about 2% from last month�s ratios. Also there are 29 negative efficiency stocks below 10 and 220 positive efficiency stocks above 10. Two months ago, there were 406 stocks above 10, so we are definitely seeing some shifting toward the negative. And remember that we had the huge positive numbers without a very large movement to the upside.

Let me give you an example of what�s showing up as positive and negative. MICC, a foreign cell phone stock, still shows up with the highest efficiency. PRSF, ANDE, TIE, and GPI round out the top five. On the negative side, DKF, WON, PQE. SGTL, and EMMS show up as great examples of negative efficiency stocks. They have nice downtrends that look like they could continue.

Incidentally, since I trade this strategy, I may or may not, have positions in the stocks that I mention. However, these examples are given for educational purposes and you should do your own due diligence if you decide to trade them.

You may have noticed that I�ve mentioned a number of these companies from month to month. After I have mentioned them, you�ll find that the price has either gone up nicely (in the case of positive efficiency stocks) or gone down nicely (in the case of negative efficiency stocks).

Part III: Our Four Star Inflation-Deflation Model.

I strongly believe that we are in an inflationary bear market and that our inflation rate is simply masked by government statistics.

So far our models have been telling us, that inflation/deflation is pretty steady, with a slight inflationary bias and that�s where secular bear markets tend to start.

So what�s our new indicator telling us about inflation?

1) The CRB Index

2) The Basic Materials Sector (XLB)

3) The London Price of Gold and

4) The Financial Sector (XLF)

Since the description of the model we�re now using is not in any of my books, I�ll continue to give it here.

1) The CRB Index. I believe that the CRB index is the one we have currently that is the least manipulated by the government. But what�s the best way to measure it? For consistency, I use two measurements.

� Is the CRB index higher than it was six months ago? If it is, we are on track for inflation.

� Is the CRB index higher than it was two months ago?

Now there are several ways to monitor these two indices.

� If both differences are higher, we�ll count one star for inflation.

� If the six-month change is higher, but the two-month change is not, then we will only count � star for inflation.

� And if both the two and six month changes are lower, then we�ll be minus one for inflation.

� However, if the six-month change is lower, while the two-month change is higher, then we�ll be minus � star for inflation. Obviously, the two minus scores will point to deflation.

2) The Basic Materials Sector ETF (XLB). In an inflationary environment, basic materials will definitely go up and this sector, to the best of my knowledge, is not manipulated by the government. Thus, we will use this sector to monitor inflation and we�ll use the same measurements use for the CRB. (1) Is the XLB higher than it was six months ago? (2) Is the XLB higher than it was two months ago? These two measurements give us four possible results.

� If both differences are higher, we�ll count one star for inflation.

� If the six-month change is higher, but the two-month change is not, then we will only count � star for inflation.

� And if both the two and six month changes are lower, then we�ll be minus one for inflation.

� However, if the six-month change is lower, while the two-month change is higher, then we�ll be minus � star for inflation. Obviously, the two minus scores will point to deflation.

3) The London PM Gold price at the end of each month. Although the government can manipulate Gold, I still like to look at monthly gold prices. However, to be consistent, we�ll use the same two measurements that we�ve used for the other indices that we are monitoring. (1) Is the price higher than it was six months ago? (2) Is the price higher than it was two months ago? Again, these two measurements give us four possible results.

� If both differences are higher, we�ll count one star for inflation.

� If the six-month change is higher, but the two-month change is not, then we will only count � star for inflation.

� And if both the two and six-month changes are lower, then we�ll be minus one for inflation.

� However, if the six-month change is lower, while the two-month change is higher, then we�ll be minus � star for inflation. Obviously, the two minus scores will point to deflation.

4) The Fourth Measurement we�ll use is related to the Financial Sector of the S&P 500.

The financial sector (XLF) tends to do well when we have deflation and poorly when we have inflation. Martin Pring, in fact, has used an index in which he divides the XLB by the XLF. Since we already use the XLB, we�ll use the XLF by itself as well. Again, we�ll use the change over six months and over two months. However, the four possible outcomes with give us a different interpretation.

� If both differences are higher, we�ll count one star for deflation (i.e., minus one for inflation).

� If the six-month change is higher, but the two-month change is not, then we will only count � star for deflation (i.e., minus � for inflation). And if both the two and six month changes are lower, then we�ll be plus one for inflation.

� However, if the six-month change is lower, while the two-month change is higher, then we�ll be plus � star for inflation. Obviously, the two minus scores will point to strong inflation.

Okay, so now let�s look at the results for the last six months.

|

Date |

CRB |

XLB |

Gold |

XLF |

| October 28th |

330.68 |

27.48 |

470.75 |

30.31 |

| November 30th |

332.49 |

29.67 |

495.85 |

31.87 |

| December 30th |

347.89 |

30.28 |

513.00 |

31.67 |

| January 31st |

363.30 |

31.74 |

568.25 |

31.95 |

| February 28th |

353.27 |

31.06 |

556.00 |

32.63 |

| March 30th |

364.70 |

32.35 |

582.00 |

32.55 |

| April 28th |

379.53 |

33.50 |

644.00 |

33.96 |

We�ll now look at the two-month and six-month changes during 2005, to see what our readings have been.

| Date | CRB2 | CRB6 | XLB2 | XLB6 | Gold2 | Gold6 | XLF2 | XLF6 | Total Score |

| April | Higher | Higher | Higher | Higher | Higher | Higher | Higher | Higher | |

| +1 | +1 | +1 | -1 | +2.0 |

The results of this model are much more sensitive (I believe) than the model I presented in Safe Strategies for Financial Freedom. The market has shown this exact same pattern for the last five months. Everything is higher over a two month period and a six month period. And thus, everything is positive for inflation except that the XLF is still increasing.

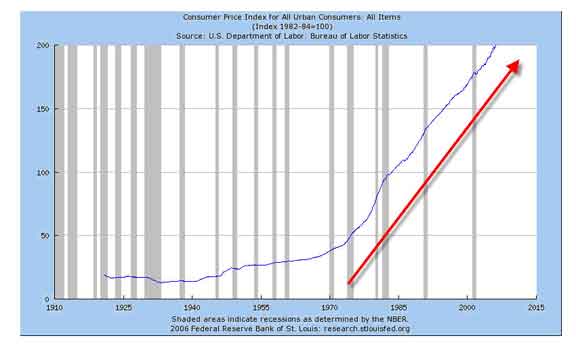

Gold and the CRB are strongly indicating inflation. Let�s look at some charts. The first figure below shows the CPI. Notice the trend since 1970. Inflation has been showing a nice steady uptrend since the 1970s. Actually, the end of the 1970s show a very strong inflationary pressure, but that�s not indicated by the government manipulated CPI which basically shows a steady growth in inflation since the 1970s. I filled my gas tank up yesterday and it cost over $3.00 per gallon. Three years ago it was less than a dollar a gallon. And energy prices affect every area of the economy.

The second figure below shows gold. Gold has been in a bear market until 2003. But look what happened in 2003. Last month I was hearing the short-term gurus tell me that gold was definitely due for a correction and even recommending put positions. And look what happened to gold last month � up over 10% in one month. Gold may be the best indicator of inflation available and it is saying that inflation in heating up.

Part IV: Tracking the Dollar.

The U.S. dollar is beginning to look weak again. Given the weak dollar and the fact that foreign stocks are BOOMING compared with the U.S. stock market, you could lose money even if the U.S. stock market does well this year. Foreign based ETFs are still strong but the strength is now shifting to Europe with Sweden (EWD), Germany (EWG), and Spain (EWP) having the highest efficiencies. Again, these are not recommendations. Do your own due diligence before investing.

Look at the next Table, showing the dollar index over the past year.

|

The Dollar Index |

|

|

Month |

Dollar Index |

|

Jan 05 |

81.06 |

|

Feb 05 |

81.81 |

|

Mar 05 |

80.89 |

|

Apr 05 |

82.23 |

|

May 05 |

83.34 |

|

June 05 |

84.95 |

|

July 05 |

85.79 |

|

Aug 05 |

84.26 |

|

Sep 05 |

83.68 |

|

Oct 05 |

85.25 |

|

Nov 05 |

86.69 |

|

Dec 05 |

85.79 |

|

Jan 06 |

84.45 |

|

Feb 06 |

85.26 |

|

Mar 06 |

85.17 |

|

Apr 06 |

84.05 |

The dollar picture is still rather mixed. However, with U.S. interest rates going high, the dollar becomes an attractive place for money to flow (as long as people believe the dollar is the same) because they can get higher rates of returns. However, the dollar is now down on the year despite high U.S. interest rates.

The most attractive place to put your money, in my book, appears to be foreign stock market ETFs, plus gold and silver stocks. IAU is now a superb ETF in terms of efficiency.

Incidentally, I have just completed revisions on the second edition of Trade Your Way to Financial Freedom. One of the changes in the new edition, which will hit the bookstores in November this year, includes analyzing newsletters that give recommendations as though they were trading systems. Just how good are they as complete systems? I think the results are rather surprising. One newsletter that costs $5,000 per year had a negative expectancy. One option newsletter editor had no idea what his results were and didn�t want us to mention his name if the results were not good (i.e., we decided not to look at option newsletters because following the performance of complex spreads or covered writes is quite complex). But some newsletters showed excellent performance.

If you have a recommendation newsletter you like (or dislike) and would like to know about it�s R-multiple distribution, let us know. If you can track the newsletter�s R-multiple distribution over at least a two year period�perhaps closing out all open positions as of March 31st, then we can tell you how that newsletter rates compared with the others we�ve been tracking.

Until the end of May update on the market�.this is Van Tharp.About Van Tharp: Trading coach, and author Dr. Van K Tharp, is widely recognized for his best-selling book Trade Your Way to Financial Fre-edom and his outstanding Peak Performance Home Study program - a highly regarded classic that is suitable for all levels of traders and investors.

|

Coming in June 2006 |

|

| Peak

Performance 101 Workshop June 3-5, 2006 |

Peak

Performance 202 Workshop June 7-9, 2006 |

|

"An absolute must

for anyone wanting to become a consistently successful trader."

Alex Rudolph

�The workshop succeeded in really pushing my limits and opening my eyes to how the world really operates�.I will never see the world the same way again.� FL, San Francisco "I met some incredibly wise, wonderful and talented people." Sara Rich "Excellent resource: A great global perspective on what is important to be a successful trader." S.S., Panama City Beach, FL |

|

The Power of Conviction, Part Iv

Conviction and Its Component Parts

by D. R. Barton, Jr.

�Conviction is worthless unless it is converted into conduct.� --Thomas Carlyle

Carlyle got it right.

The trading and investing world is full of folks who will give you their opinion and argue vehemently for their point of view. But few and far between are those rare individuals who turn those convictions into action (or conduct as Mr. Carlyle said).

I�ve been blathering on about Ken Long�s ability to build absolute conviction in himself and his trading style and then parlay that conviction into decisive action. In this series of articles, I have tried to break down the source of Ken�s conviction, which I enumerated as follows:

1. Observe a potentially repeatable event in the market.

2. Check to see if the events fit within your belief structure about the markets.

3. Break the event down into component parts.

4. Quantify the component parts.

5. Build a system from those components.

6. Test the system on historical data.

7. Test the system in real-time, with real money.

8. Trade the system.

9. Monitor the system against performance benchmarks.

Today we�ll tackle the middle three.

Quantify the component parts. For many folks, this is one of the toughest tasks of system building. Once you�ve spotted a situation that repeats itself and figured out the main drivers, you have to put numbers that makes sense to those drivers (indicators). Here�s where people make two key mistakes:

Failing to match their indicator�s time frame with the trade�s expected time frame. All too often, someone wants to enter a three day trade and they�ll use a 200 day moving average to determine trend direction. If you�re looking to catch a short, or intermediate, term trend, then use a trend indicator designed for those time frames!

Developing an indictor based on back testing instead of market logic. �I was looking to time my entries better and found that if I only took the trade on the third Tuesday of the month after high tide, the winning percentage went up drastically!� Ouch. I�ve heard less inane but equally implausible arguments based on back testing. To avoid this problem, always make sure that you ask this question, �Does this indicator make sense in market terms? Does it fit the beliefs upon which the system is based?�

Build a system from those components. You�ve found a great set-up. Now build a system around that set-up. Too often, we�re tempted to jump in a try out an entry with real money before we have a complete system to guide the whole strategy. Add an entry signal, a stop loss, re-entries, profit taking exits, and position sizing. Only then are your ready to move on.

Test the system on historical data. Some people put too much emphasis on this step. Others don�t put enough. But to gain confidence in your strategy, a well designed series of back tests can really help. Make sure you incorporate these two key elements into your tests:

Multiple market conditions. People routinely discuss what a statistically significant sample is for a back test, and that is partially to make sure that you�re using good science as a basis for your testing, but it is also important to help insure that you cover a range of different market conditions. In general, the shorter your trading timeframe, the more testing data you need. If you have a system that trades five times a day, a back test of 100 trades doesn�t mean that much because it only covers a month�s time and probably doesn�t include many different market environments. On the other hand, a long-term system may only trade five times a year. For that system, a back-test of 30 � 50 trades is probably quite sufficient.

Avoid curve-fitting and over-optimization. Much has been written on this, so I won�t belabor the subject here. For a good overview of the topic, check out this link: http://www.investopedia.com/articles/trading/05/030205.asp .

Next week we�ll begin looking at how Ken transitions a system into the real world. Until then�

Great Trading!

D. R.

D. R. Barton, Jr. is the Chief Operating Officer and Risk Manager for the Directional Research and Trading hedge fund group. D. R. has been actively involved in trading, researching, and teaching in the markets since 1986. D. R. has taught extensively in many investment areas including intra-day trading, swing trading, and cutting edge risk management techniques.

His writing credits include co-authoring Safe Strategies for Fin-ancial Fre-edom and co-creator and contributing author on Fin-ancial Fre-edom Through Electronic Day Trading.

D.R. presents the IITM Swing Trading Workshop and Professional Tactics for Day Traders Workshop. Each workshop is only held once each year.

For Our German Language Readers:

Van Tharp is the Keynote Speaker

Technische Analyse Kongress 2006

Frankfurt � May 20, 2006

Als Mitglied des Van Tharp Institutes erhalten Sie 20% auf den Seminarpreis !

Expectancy Vs Money Management

Author: oem7110

Date: 04-18-06 21:05

Would anyone like to share any idea on how to select the trading strategies based on expectancy vs money management?

For comparing strategies, I always select the one with highest expectancy, but when I also need to consider position sizing into the selection criteria, then I don't know what to do?

Does anyone know on how to balance between expectancy and money management [the size of position] in order to select the best strategy for trading?

Thank you for any suggestion

Eric

Reply To This Message

Re: Expectancy Vs Money Management

Author: PMK

Eric,

Position-sizing is like the volume control on your HiFi - it can make the sound louder or quieter but it can't change the music. Position-sizing should not be a factor in strategy selection - only in tuning the strategy to meet your objectives.

Expectancy + Trade Frequency + Position Sizing determine your likely reward and your likely drawdown profile overall.

I have found that simulation is the most effective way of testing any combination (of trading system + position sizing) to see how it matches your objectives.

Hope this helps

Special Reports By Van Tharp

Click below to read page one of each report, or to order.

Do Not Reply to this email using the reply button as the email address is not monitored, your email will not be seen. Please click this link to contact us: [email protected]

The Van Tharp Institute does not support spamming in any way, shape or form. This is a subscription based newsletter.

If you no longer wish to subscribe, Unsubscribe Here

Or, paste this address in your browser: http://www.iitm.com/privacy_policy.htm

The Van Tharp Institute

102-A Commonwealth Court, Cary, NC 27511 USA

800-385-4486 * 919-466-0043 * Fax 919-466-0408

Copyright 2006 the International Institute of Trading Mastery, Inc.